What we cover

The start of the new year usually brings renewed optimism for fuel retailers who have put the slow holiday period behind them. This particular January, however, didn’t bring the kind of good news that retailers usually look for.

A rough slate of weather and new international sanctions from the departing Biden administration combined to negatively affect margins, fuel demand, and c-store foot traffic. Though with every turn of the calendar, retailers get closer to the high-demand spring and summer months.

Dive into our latest update on American fuel trends — including a closer look at the movement in diesel fuel.

Last month’s data

Cold weather and sanctions put a damper on the industry

Though last month was the hottest January on record across the globe, America experienced a brutal cold wave that suppressed fuel demand. Generally speaking, January usually has the lowest levels of daily traffic for fuel stations, but 2025 started at an especially low point.

Last month, average daily fuel transactions were down just over 4% from December 2024, and convenience store transactions were down nearly 6% over that same period. Stations and stores in Western states saw the best performance in January, but there were no real winners in the month — just losers and bigger losers. Out West, declines were more modest and in line with seasonal expectations. The declines in fuel traffic and convenience traffic were 1.7% and 3%, respectively.

With cold weather doing a number on demand, international sanctions similarly affected supply. In the final days of his administration, President Biden issued new sanctions on Russian oil exports. That action led to a rise in global crude prices and increased shipping costs.

Refineries also impacted fuel in the way they responded to January’s demand trends. Because of lower demand from the cold weather, some refineries started their seasonal maintenance earlier than usual. With those refineries producing less fuel in January, the supply of wholesale fuel decreases and its rack price increases.

Together, these factors contributed to an increase in rack prices across the board. Nationally, rack prices increased by about 12 cents per gallon of regular, and roughly half of that increase (about 7 cents per gallon) was passed onto consumers in the form of higher sign prices. In all, retailers gave up margin in the face of lower demand, profiting about 5 fewer cents per gallon of regular than they had last month.

The largest jump in rack prices came from the West — where prices were up 18 cents per gallon — and yet, over that same period, sign prices only increased by 3 cents per gallon. The largest increase in rack prices and the smallest increase in sign prices meant that Western retailers saw the most substantial impact to margins in January.

A deep dive into diesel

We track over 40 variables related to fuel and convenience every month; in January, the trends of diesel fuel warrant closer inspection. But first, some context is required.

In the winter, many American households burn heating oil to stay warm. Both diesel and heating oil are middle distillates. Chemically, that means they come from the same fraction of a crude oil barrel. Economically, it means that demand (and thus, prices) for each product is intrinsically tied together; when demand increases the price for one of the products, a similar effect occurs for the other.

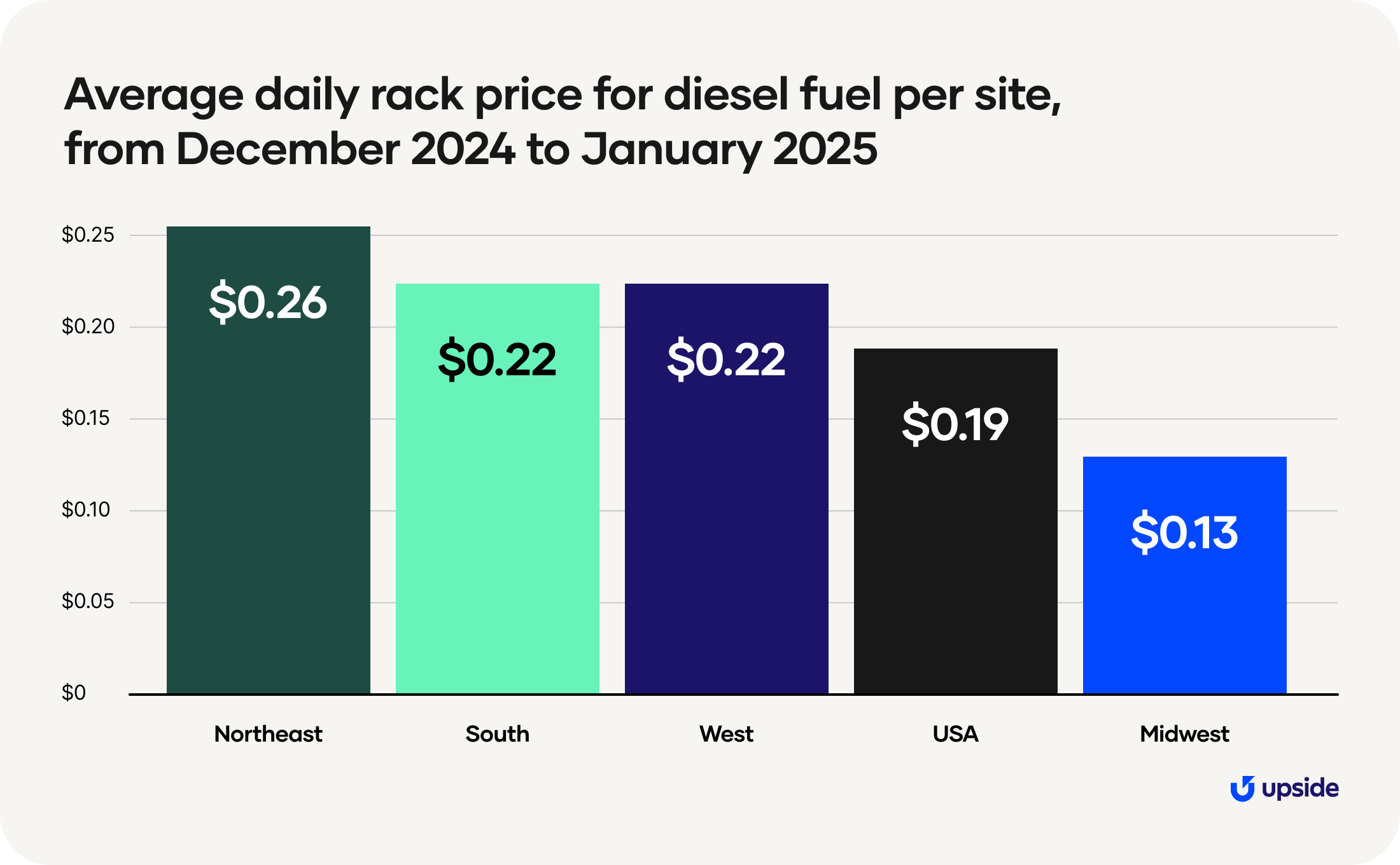

Due to the cold weather last month, demand for heating oil was higher as Americans burned more of it to keep warm. Based on the above economic principles, we know that causes a similar increase in demand for diesel. And indeed, the average station saw daily diesel rack prices increase by nearly 20 cents per gallon in January.

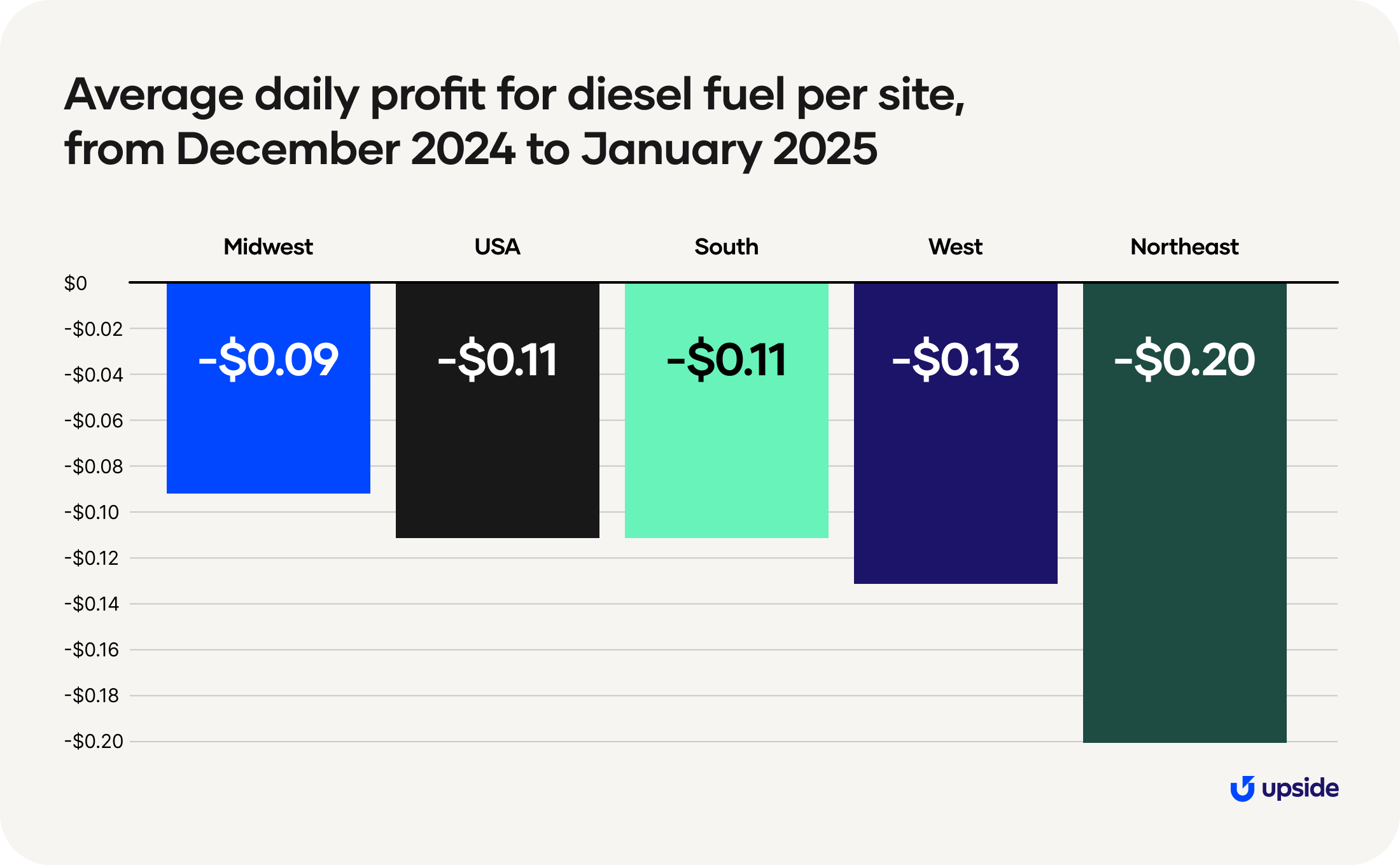

Similar to the trend in regular fuel, the average American station only passed on an increase of 8 cents per gallon onto the diesel sign price — and as such, diesel margins at the average station were 11 cents per gallon in January than in December. This indicates stations absorbed a significant portion of the cost increase themselves.

During the week of January 13 in particular, diesel margins dipped 24 cents per gallon — that’s their lowest level since September 2023. Given that diesel margins have been on a steady decline over the past two years (and that diesel has been an area of significant investment over the past decade), this information is concerning for brands and retailers alike.

Predictions and considerations

Warmer weather will help demand, but refinery maintenance stands in the way of better margins

With milder temperatures projected for February, demand may increase, but retailers expecting margin relief might have to wait a few more months. Continued refinery maintenance will likely play a larger role in keeping rack prices high.

As springtime approaches, so does the annual switchover from the winter blend to the summer blend of gasoline. This usually starts taking place in March in some regions of the country, completing in April in time for peak driving season. Right before the switch occurs, some stations and regions might experience short-lived sign price discounting in February or March as they clear out winter-blended gasoline from their tanks.

Of course, there’s also the elephant in the room: the looming threat of American tariffs on Canadian crude imports. Additionally, as long as the sanctions on Russian exports remain in place, fuel prices will remain slightly elevated.

Potential tailwinds:

- February brings us another month closer to springtime, when warmer weather attracts more people to the road and increases fuel demand.

Potential headwinds:

- Though a deal was reached to delay the implementation of the 10% tariffs on Canadian energy imports in early February, these tariffs are currently scheduled to go into effect in March. The associated policy uncertainty could destabilize the market.

- Rack prices will increase in March and April due to the switch to summer-blend fuel.

- While they conduct annual maintenance, refineries will be producing less fuel, thereby decreasing supply and increasing rack prices.

Want a closer look at the data?

Check out our insights hub with all our fuel and convenience monthly updates, plus special industry reports.